Imagine you manage facilities for a mid-size hotel chain. You've been hearing about cashierless checkout, autonomous vending, frictionless retail, the terms are everywhere at industry conferences. You want to evaluate whether it makes sense for your properties.

So you do what every buyer does before they talk to a single vendor: you search.

You type "autonomous checkout for hotels" into Google. You ask ChatGPT "what's the best cashierless retail solution for hospitality." You scroll through the results, open a few tabs, read a few articles.

Here's what you find: almost nothing from the companies actually building this technology.

What you do find is a blog from a small player most industry insiders haven't heard of, covering vending machine costs, placement strategies, ROI guides, gym vending, school vending, hotel retail. Article after article, ranking after ranking, cited in AI responses, appearing in Google's AI Overviews.

This is the strange reality of the autonomous retail market in 2026. It is one of the fastest-growing segments in all of technology, a projected expansion from $27 billion to $74 billion by 2035, serious venture capital, IIT founders, partnerships with Aldi and major stadiums. And yet, when the buyers it desperately needs to reach go looking for information, most of the industry simply isn't there.

A Market at an Inflection Point

The logic of autonomous retail has never been stronger. Labour costs are rising. Retail theft is up sharply since 2019, with the National Retail Federation's most recent security surveys placing shrink-related losses near record highs. The U.S. Bureau of Labor Statistics continues to report persistent vacancies in food preparation and service occupations running into the seven figures. The economics of staffed checkout in small-format environments, corporate breakrooms, hotel lobbies, university dorms, gym concessions, simply don't work anymore.

The technology has matured in parallel. Computer vision systems can now track products and customers in real time without biometric data, processing everything locally on edge hardware to satisfy increasingly strict privacy regulations. The "Just Walk Out" concept that Amazon first made famous has been reengineered for sub-500-square-foot deployments, offered on a Retail-as-a-Service (RaaS) model that eliminates the capital expenditure that previously made adoption unthinkable for smaller operators.

The convergence of economic pressure and technological readiness has created a classic adoption window. Several well-funded companies are racing to establish category leadership. The race is being fought in boardrooms, at trade shows, and through enterprise sales teams, while the digital channel, the place where the buyer's journey now begins, has been almost entirely abandoned.

What does the autonomous-retail AI-visibility data actually show?

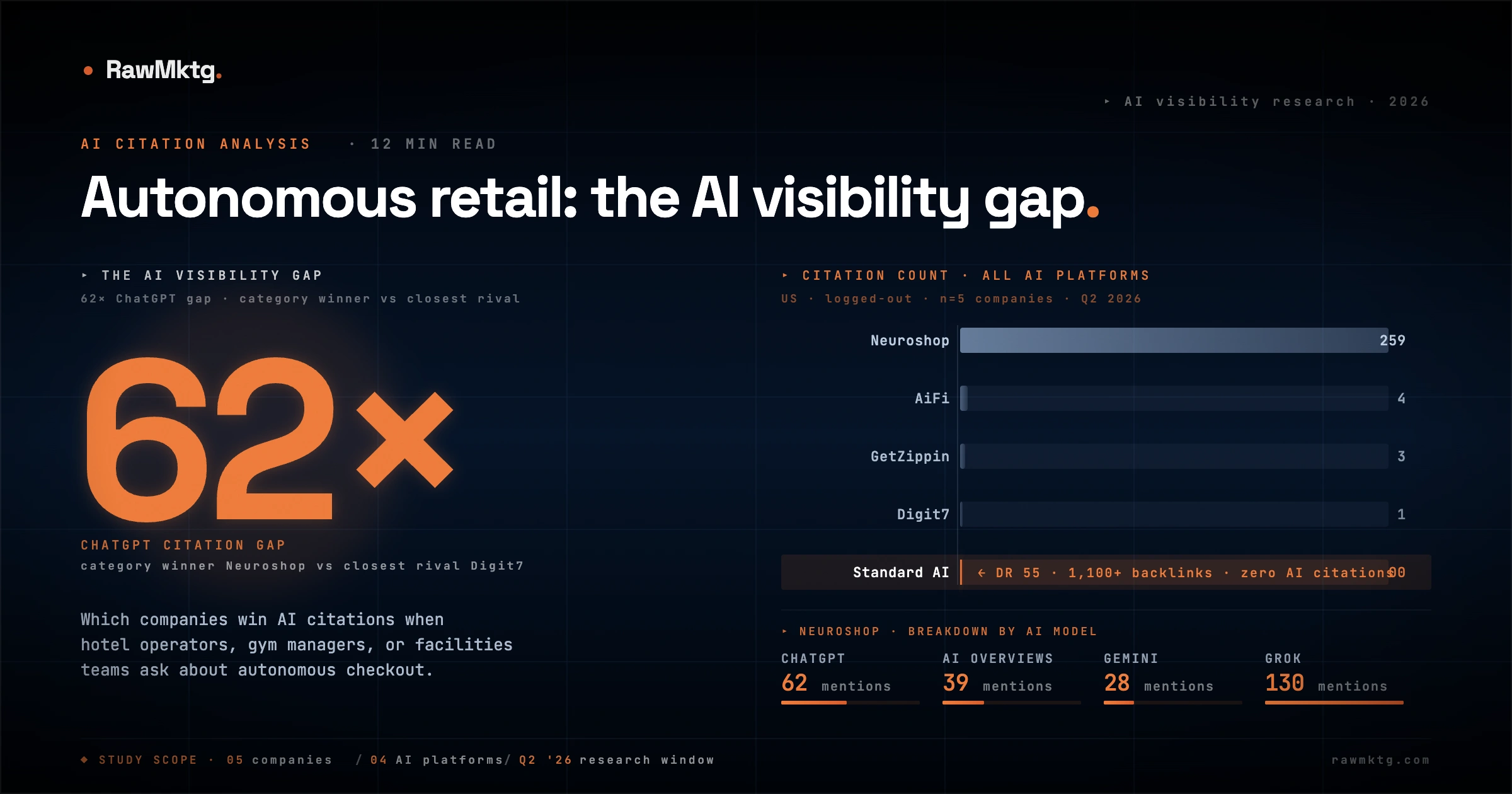

Five leading players in the autonomous checkout and smart retail space: AiFi, Standard AI, GetZippin, Digit7, and Neuroshop. A quick note on metrics: Domain Rating (DR) is Ahrefs' 0–100 measure of how much the web's link graph trusts a site. Both DR and referring domain counts are leading indicators of search performance, which makes the findings below counterintuitive.

AiFi is arguably the most credentialed company in the group. DR of 60, 636 referring domains, a partnership with Aldi, and deployments across stadiums and workplaces globally. In traffic terms: approximately 820 visits per month, 19 keywords ranked, 4 AI Overview citations, zero ChatGPT citations.

Standard AI, with a DR of 55 and over 1,100 referring domains built up over years, generates around 174 organic visits per month and ranks for 7 keywords. Traffic has been in measurable decline for the past 12 months, dropping from roughly 280 visits/month toward 170. Zero AI citations across any platform.

GetZippin, the checkout-free technology firm that has powered cashierless concessions in stadiums, airports, and universities across five continents, pulls in approximately 170 organic visits per month and ranks for 22 keywords. Also in decline, from a peak of around 340 visits/month a year ago. One AI Overview citation. Two on ChatGPT.

These are not obscure companies. These are funded, deployed, press-covered technology providers with years of market presence and link profiles any early-stage startup would envy. And yet the buyer who goes looking for information in their category will not encounter them.

| Metric | Neuroshop | Digit7 | AiFi | GetZippin | Standard AI |

|---|---|---|---|---|---|

| Domain Rating | 16 | - | 60 | - | 55 |

| Organic keywords | 274 | ~est. growing | 19 | 22 | 7 |

| Monthly organic visits | ~1,800 | ~1,800 | ~820 | ~170 | ~174 |

| ChatGPT citations | 62 | 1 | 0 | 2 | 0 |

| AI Overview appearances | 39 | - | 4 | 1 | 0 |

| 12-month traffic trend | 9× growth | ~18× growth | Flat | Declining | Declining |

Source: Ahrefs, May 2026. Traffic = estimated monthly organic visits. DR = Domain Rating (Ahrefs 0–100 scale).

Which autonomous-retail company cracked AI visibility?

Neuroshop has a Domain Rating of 16. Its referring domain count of 333 is respectable but not exceptional. By the authority metrics the SEO industry treats as leading indicators of success, it should be invisible.

It is not invisible.

The mechanism is not mysterious. Neuroshop has done something its better-funded, higher-authority competitors have not: it publishes content that maps directly to the questions buyers ask before they start evaluating vendors. Questions like: How much does a vending machine cost? Where should I place a vending machine? What are the best smart vending solutions for gyms? How does AI vending actually work?

These are low-competition queries with clear buyer intent. The average keyword difficulty score across Neuroshop's top-ranking terms sits between 0 and 5, meaning almost any site with a reasonable domain authority could rank for them, if someone simply wrote the page.

Nobody else did. Neuroshop did. And now it appears in AI responses over 100 times while companies with four times its domain authority appear zero times.

Digit7: The Second Mover Catching Up Fast

Neuroshop is not alone in recognising the opportunity. Digit7, a direct competitor offering autonomous stores, AI-powered smart coolers, and frictionless checkout, has been investing in product-specific content pages: dedicated landing pages for "AI vending machines," "smart cooler," and "frictionless retail technology."

The results are visible in the traffic data. Twelve months ago, Digit7 was generating roughly 100 organic visits per month. By May 2026, that figure has reached approximately 1,800: almost identical to Neuroshop's current volume.

But the routes are genuinely different, and the difference is instructive. Neuroshop is winning informational, top-of-funnel queries, the cost guides, the placement explainers, the "how does AI vending work" pages that capture buyers months before they're ready to evaluate. Digit7 is winning mid-funnel product queries, "smart cooler," "AI vending machine," "frictionless retail" searches from buyers who already know what category they want and are comparing options. Same destination, different points in the buyer journey, both currently uncontested.

What is AI search doing to the autonomous-retail market?

The traditional SEO story here would be straightforward: companies that publish content get traffic, companies that don't, don't. But there is a second dimension emerging that makes the stakes considerably higher.

AI-powered search, ChatGPT, Perplexity, Google's AI Overviews, Microsoft Copilot, Grok, is rapidly becoming the first stop in the B2B buyer journey. When a hotel procurement manager, a university facilities director, or an office building operator begins evaluating autonomous retail technology, a meaningful and growing proportion of them are starting by asking an AI assistant rather than typing a query into traditional search.

The citation mechanisms behind these tools differ in important ways. Google's AI Overviews draw heavily on the same index that powers traditional search. ChatGPT's retrieval pipeline pulls from a different mix, with a known bias toward Reddit, Wikipedia, G2-style review platforms, and high-authority editorial sources. Perplexity weights live web results more heavily than either.

What is consistent across them: every one of these systems rewards brands with substantive, well-structured content distributed across the kinds of sources their retrieval pipelines trust. The brand that shows up in AI responses is, almost without exception, the brand with the content infrastructure to support it. Not only is there a current-day traffic gap between content-investing companies and those that aren't, there is a compounding future disadvantage. As AI search behaviour grows, the companies that have not built content infrastructure today will find themselves increasingly invisible to buyers who never even reach a traditional search results page.

Why the Established Players Are Vulnerable

In most technology categories, the companies with the highest domain authority, the most backlinks, and the longest history of press coverage would be expected to dominate organic and AI search. Authority compounds. History matters.

In autonomous retail, that advantage has not translated. AiFi (DR 60) is being outranked and out-cited by Neuroshop (DR 16). Standard AI (DR 55, 1,100 referring domains) generates less search traffic than a company a fraction its size that simply started writing.

The reason is straightforward but often misunderstood: domain authority is a precondition for ranking, not a guarantee of it. A high-authority domain with no content targeting any particular query will not rank for that query. A lower-authority domain with well-written, properly structured content targeting a low-competition query will often rank above it.

The established players have accumulated authority through press coverage, product launches, and investor announcements. That authority is real and valuable. But it has been sitting undeployed, a loaded weapon pointed at no particular target. The content infrastructure to convert that authority into search traffic and AI citations simply hasn't been built.

This creates a window for newer entrants that is unusual in technology markets. The moat that incumbents would typically hold is not protecting them because it has not been activated.

A Note on Grabango

Grabango is worth a brief mention because it complicates this narrative in an honest way. The company raised over $93 million, partnered with Aldi, 7-Eleven, and Circle K, and shut down in late 2024. The post-mortems pointed to unit economics, high-CapEx retrofits that retailers ultimately preferred to replace with cheaper self-checkout kiosks, and a tightening funding environment that punished slow deployment growth.

Content distribution would not have saved Grabango. The problem was that the product was too expensive for the buyers it was reaching. No amount of blog traffic fixes that.

But Grabango's failure does sharpen one point. A business that depends entirely on enterprise sales relationships to add deployments is structurally exposed when those relationships slow, and they slow for reasons that have nothing to do with product quality. The current generation of RaaS-model players is selling to a structurally different market: smaller, more numerous operators who research independently and convert through digital channels. That market is reachable through content in a way the old enterprise-only motion was not. Distribution diversity is a hedge against the specific kind of slowdown that took Grabango down, not a substitute for unit economics.

The Review Platform Gap

There is one more dimension to this visibility gap that does not show up in traditional SEO metrics but is increasingly consequential for AI citation volume: the presence (or absence) of a brand on review and comparison platforms.

G2, Capterra, and GetApp collectively function as primary citation sources for AI responses about B2B technology products. When someone asks ChatGPT "what is the best autonomous checkout solution," the models pull heavily from these platforms because they contain structured, verified information about products in comparative context.

Among the autonomous retail players covered in this analysis, presence on these platforms ranges from thin to nonexistent. This is not a hard problem to solve, creating and optimising a G2 or Capterra listing is a matter of hours, not months. But the compounding effect of having verified customer reviews indexed on a high-authority platform, cited by AI models, and linked back to a product page is significant.

Reddit carries a similar weight in AI training data that is frequently underappreciated. Several subreddits, r/vending, r/retailtech, r/smallbusiness, contain active discussions about autonomous retail technology. Brands that participate in those conversations authentically are building citation equity that search analytics tools don't easily measure but AI models treat as signal.

What To Do About It

The diagnosis above translates into a fairly compressed set of moves. The order matters.

Before any content investment, build the list of questions a hotel facilities manager, a university procurement officer, a stadium operations lead, or a corporate workplace director is actually typing into Google and ChatGPT. The cost questions. The placement questions. The "how does this compare to vending" questions. The integration questions. Most of these queries have keyword difficulty scores in the single digits today. They will not stay that way.

This is a matter of hours, not a strategic initiative. The compounding citation effect in AI responses begins the moment a listing exists with real reviews against it.

r/vending, r/retailtech, r/smallbusiness, r/restaurateur. Authentically, with the brand attached, answering questions. Not posting press releases. ChatGPT's retrieval pipeline gives Reddit disproportionate weight, this is the highest-leverage hour of work most companies in this category are not doing.

Clear H2s framed as the question being answered. Direct answers in the first sentence under each heading. Schema markup. Comparison tables. The same content can rank in traditional search and get cited in AI Overviews, but only if it's structured for both.

Digit7's playbook is the proof. A page titled "AI Vending Machine" that actually explains the category, the use cases, and the buying considerations will outrank a page titled "Our Product" that explains nothing.

None of these are expensive. The category is wide open precisely because nobody is doing them.

What the Next 12 Months Will Look Like

The autonomous retail market is at a particular moment where small investments in digital presence can produce disproportionate returns. The category keywords are undercontested. The content gaps are large and obvious. The companies currently winning, Neuroshop, and now Digit7, have demonstrated the playbook conclusively.

The 365 Retail Markets and Cantaloupe merger, completed earlier this year in an $848 million deal, creates a giant in the unattended retail space with 1.34 million managed devices globally. Scale at that level brings sales infrastructure, press coverage, and brand recognition. What it rarely brings quickly is the kind of nimble, buyer-journey-mapped content operation that wins at search and AI.

The window for category content leadership is open now. It will not stay open indefinitely. As more players recognise the gap and begin investing, keyword difficulty will rise, AI citation competition will intensify, and the cost of acquiring the same positions will increase. The same dynamic is visible in our India cross-border payments backlink analysis: brands that built broad adjacent-topic footprints early hold structural advantages that newer entrants must work around.

The buyers are searching. They are asking AI assistants. They are reading the content that appears. The question is simply who wrote it.

How large is the autonomous retail market and which companies lead it?

The autonomous retail market is projected to grow from $27 billion to $74 billion by 2035, driven by cashierless checkout, smart vending, and AI-powered inventory management. Key players include AiFi, Standard AI, GetZippin, Neuroshop, and Digit7. Despite significant venture capital and enterprise deployments at major retailers and stadiums, most companies have minimal organic search presence and near-zero AI citation visibility.

Which autonomous retail company has the most AI citations?

Neuroshop, with a Domain Rating of just 16, leads the competitive set in ChatGPT citations, outperforming AiFi (DR 60), Standard AI (DR 55), and GetZippin despite having a fraction of their domain authority. Neuroshop's citation advantage comes from content architecture: its pages are structured as retrievable answer units, with specific claim-level sourcing that AI engines can verify and cite independently of domain authority signals.

Why do AiFi and Standard AI have low AI visibility despite high domain authority?

AiFi (DR 60) has 4 Google AI Overview citations and zero ChatGPT citations despite a partnership with Aldi and global deployments. Standard AI (DR 55) has zero AI citations across all platforms. Both companies' sites rely on narrative marketing copy and client-side rendering, content human readers understand but that AI retrieval crawlers cannot parse. High domain authority does not transfer to AI citation eligibility without structural content optimization.

What is the most important content fix for autonomous retail vendors?

The highest-ROI fix is rebuilding product and use-case pages as answer-lead content that begins with a direct response to the buyer's question in the first 60 words. Category queries like 'what is cashierless checkout technology' and 'how does autonomous retail work' represent the entry point of the buying journey. Vendors not appearing in AI answers to these queries are absent from consideration before the sales cycle begins.

rawmktg. publishes data-driven research on B2B marketing strategy, SEO, GEO, and AI search visibility for SaaS companies. Contact: vinayak@rawmktg.com